With November’s election fast approaching, the Republican candidates seeking to challenge President Barack Obama claim that his policies have done nothing to support recovery from the recession that he inherited in January 2009. If anything, they claim, his fiscal stimulus made matters worse. And, despite recent improvement, the level of unemployment indeed remains far too high. They do not blame George W. Bush for the recession that began two months after he took office in 2001. There hadn’t yet been time for bad policies to damage the economy.)

Obama’s Democratic defenders counter that his policies staved off a second Great Depression, and that the US economy has been steadily working its way out of a deep hole ever since. Middle-ground observers, meanwhile, typically conclude that one cannot settle the debate, because one cannot know what would have happened otherwise.

There is a good case to be made that government policies - while not strong enough to return the economy rapidly to health — did indeed halt an accelerating economic decline. By “government policies,” I mean not just the fiscal stimulus the new president steered through Congress when he took office, but also the Obama version of TARP, and Fed Chairman Ben Bernanke’s aggressive monetary stimulus. All three policy initiatives remain extremely unpopular with Republicans, and ambiguous among swing voters.

But the middle-ground observers are of course right that one cannot prove what would have happened otherwise. It is also true that it is rare for a government’s policies to have a major impact on the economy immediately. These things usually take time. One cannot infer the merit of a new president’s policies from the path of the economy during his first few months in office. (For example, I did

But here is the remarkable thing: whether one listens to the Republicans, the Democrats, or the middle-ground observers, one gets the impression that the economic statistics show no discernible improvement around the time that Obama took office. In fact, the reality could hardly be more different.

This is especially true if one looks at revised economic statistics, which show the US economy to have been in far worse shape in January 2009 than was reported at the time. In January 2009, the annualized growth rate in the second half of 2008 was officially estimated to have been negative 2.2%; but current figures reveal it to have been a horrendous negative 6.3%. This is the main reason why the level of economic activity in 2009 and 2010 was so much lower than had been forecast, which in turn explains why unemployment was so much higher.

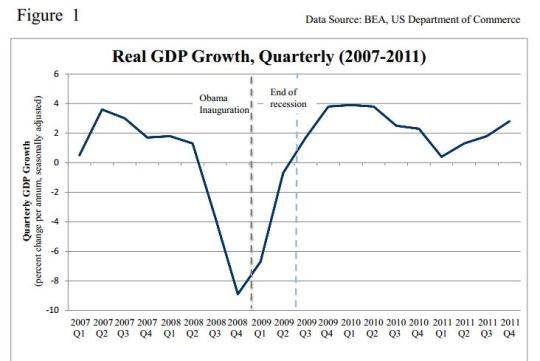

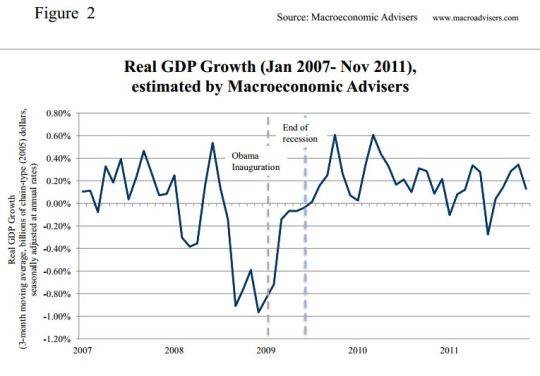

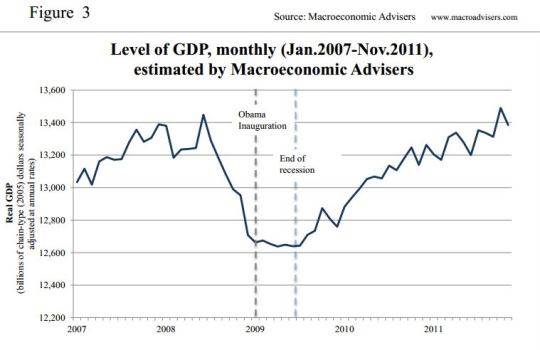

Figure 1 shows the quarterly economic growth rate. The maximum rate of contraction — a veritable freefall in the economy — came in the last quarter of 2008 (the quarterly GDP data come from the Bureau of Economic Analysis of the U.S. Commerce Department). More specifically, it came in December, according to the monthly GDP estimates from the highly respected MacroAdvisers. (See monthly income figures in the form of growth rates in Figure 2 or levels of GDP in Figure 3.) This was the month before Obama was inaugurated. The situation miraculously began to improve as soon as Obama’s term began!

(Click here for larger graphs)

The full force of the fiscal stimulus package began to go into effect in the second quarter of 2009. The NBER officially designates the end of the recession as having come in June of that year. GDP growth turned positive in the third quarter.

US economic growth slowed down again in late 2010 and early 2011, as one can see in Figure 1. The timing coincides with the beginning of withdrawal of the Obama fiscal stimulus. Indeed, the government has been the one sector to experience contraction in income and employment over the most recent five quarters. The private economy has been expanding.

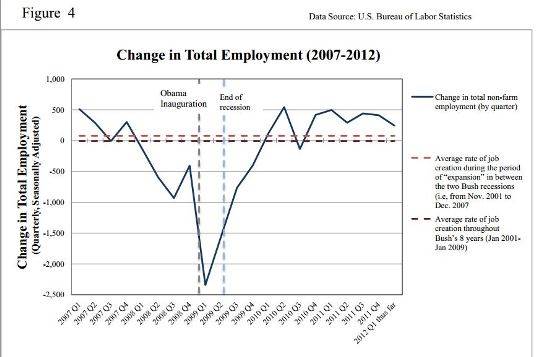

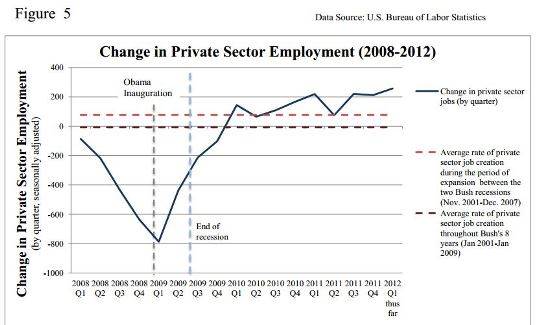

Other economic indicators, such as interest-rate spreads and the rate of job loss, also turned around in early 2009. Labor-market recovery normally lags behind that of GDP - hence the “jobless recoveries” of recent decades. But the graph of monthly job losses and gains reveals that here, too, the end of the freefall came precisely when Obama was inaugurated. The last two charts show the same “V” shaped pattern in the monthly job change figures that are released by the Bureau of Labor Statistics, as the GDP growth figures that are released by the BEA. The rate of job growth over the last two years, inadequate as it is, actually exceeds the rate of job growth during the Bush Administration, even if one counts only the period before the big recession hit in December 2007.

Again, these graphs do not demonstrate that Obama’s policies yielded an immediate payoff. In addition to the lags in policies’ effects, many other factors influence the economy every month, making it difficult to disentangle the true causes underlying particular outcomes.

What is the right way to assess whether the fiscal stimulus enacted in January 2009 had a positive impact? Start with common sense. When the government spends $800 billion on such things as highway construction, teachers and policemen who were about to be laid off, and so on, it has an effect. Workers who would otherwise not have a job now have one. Furthermore, they may spend some of their income on goods and services produced by other people, creating a multiplier effect.

Those who claim that this spending does not boost income and employment (or that it even hurts), apparently believe that as soon as a teacher is laid off, a new job is created somewhere else in the economy, or even that the same teacher finds a new job right away. Neither can be true, not with unemployment so high and the average spell of unemployment much longer than usual.

They also think that the government deficit drives up inflation and interest rates, thereby crowding out other spending by consumers and firms. But interest rates are rock bottom, even lower than they were in January 2009, while core inflation is running at its lowest levels since the early 1960’s. The conditions of the last four years - high unemployment, depressed output, low inflation, and low interest rates - are precisely those for which traditional “Keynesian” remedies were designed.

Economists’ more sophisticated forecasting models also show that the fiscal stimulus had an important positive effect, for much the same reasons as the common-sense approach. The non-partisan US Congressional Budget Office reports that the 2009 spending increase and tax cuts gave a positive boost to the economy, and indeed had the extra multiplier effects of the traditional Keynesian models. Allowing for a wide range of uncertainty [to allow for different economists' views], the CBO estimates that the stimulus added 1.5 percent to 3.5 percent to the level of GDP by the fourth quarter, relative to where it otherwise would have been. The boost to 2010 GDP, when the peak effect of the stimulus kicked in, was roughly twice as great.

To be sure, of the many theoretical models produced by eminent macroeconomists at prestigious universities, some say that fiscal stimulus has no positive effect on the economy, even under recent economic conditions. (The theoretical innovations underlyng the models have even won Nobel Prizes for the innovators, and not without justice.) But these models are not sufficiently realistic to meet the market test: they are not used by private businessmen for whom getting good forecasts matters to their planning and in turn to the success of their businesses.

Of course, econometric models do not much interest the public at large. A turnaround needs to be visible to the naked eye to impress voters. Given this, one can only wonder why basic charts, such as the 2008-2009 “V” shape in growth, have not been used - and reused - to make the case.

(Click here for larger graphs)

With November’s election fast approaching, the Republican candidates seeking to challenge President Barack Obama claim that his policies have done nothing to support recovery from the recession that he inherited in January 2009. If anything, they claim, his fiscal stimulus made matters worse. And, despite recent improvement, the level of unemployment indeed remains far too high. They do not blame George W. Bush for the recession that began two months after he took office in 2001. There hadn’t yet been time for bad policies to damage the economy.)

Obama’s Democratic defenders counter that his policies staved off a second Great Depression, and that the US economy has been steadily working its way out of a deep hole ever since. Middle-ground observers, meanwhile, typically conclude that one cannot settle the debate, because one cannot know what would have happened otherwise.

There is a good case to be made that government policies - while not strong enough to return the economy rapidly to health — did indeed halt an accelerating economic decline. By “government policies,” I mean not just the fiscal stimulus the new president steered through Congress when he took office, but also the Obama version of TARP, and Fed Chairman Ben Bernanke’s aggressive monetary stimulus. All three policy initiatives remain extremely unpopular with Republicans, and ambiguous among swing voters.

But the middle-ground observers are of course right that one cannot prove what would have happened otherwise. It is also true that it is rare for a government’s policies to have a major impact on the economy immediately. These things usually take time. One cannot infer the merit of a new president’s policies from the path of the economy during his first few months in office. (For example, I did

But here is the remarkable thing: whether one listens to the Republicans, the Democrats, or the middle-ground observers, one gets the impression that the economic statistics show no discernible improvement around the time that Obama took office. In fact, the reality could hardly be more different.

This is especially true if one looks at revised economic statistics, which show the US economy to have been in far worse shape in January 2009 than was reported at the time. In January 2009, the annualized growth rate in the second half of 2008 was officially estimated to have been negative 2.2%; but current figures reveal it to have been a horrendous negative 6.3%. This is the main reason why the level of economic activity in 2009 and 2010 was so much lower than had been forecast, which in turn explains why unemployment was so much higher.

SUMMER SALE: Save 40% on all new Digital or Digital Plus subscriptions

Subscribe now to gain greater access to Project Syndicate – including every commentary and our entire On Point suite of subscriber-exclusive content – starting at just $49.99

Subscribe Now

Figure 1 shows the quarterly economic growth rate. The maximum rate of contraction — a veritable freefall in the economy — came in the last quarter of 2008 (the quarterly GDP data come from the Bureau of Economic Analysis of the U.S. Commerce Department). More specifically, it came in December, according to the monthly GDP estimates from the highly respected MacroAdvisers. (See monthly income figures in the form of growth rates in Figure 2 or levels of GDP in Figure 3.) This was the month before Obama was inaugurated. The situation miraculously began to improve as soon as Obama’s term began!

(Click here for larger graphs)

The full force of the fiscal stimulus package began to go into effect in the second quarter of 2009. The NBER officially designates the end of the recession as having come in June of that year. GDP growth turned positive in the third quarter.

US economic growth slowed down again in late 2010 and early 2011, as one can see in Figure 1. The timing coincides with the beginning of withdrawal of the Obama fiscal stimulus. Indeed, the government has been the one sector to experience contraction in income and employment over the most recent five quarters. The private economy has been expanding.

Other economic indicators, such as interest-rate spreads and the rate of job loss, also turned around in early 2009. Labor-market recovery normally lags behind that of GDP - hence the “jobless recoveries” of recent decades. But the graph of monthly job losses and gains reveals that here, too, the end of the freefall came precisely when Obama was inaugurated. The last two charts show the same “V” shaped pattern in the monthly job change figures that are released by the Bureau of Labor Statistics, as the GDP growth figures that are released by the BEA. The rate of job growth over the last two years, inadequate as it is, actually exceeds the rate of job growth during the Bush Administration, even if one counts only the period before the big recession hit in December 2007.

Again, these graphs do not demonstrate that Obama’s policies yielded an immediate payoff. In addition to the lags in policies’ effects, many other factors influence the economy every month, making it difficult to disentangle the true causes underlying particular outcomes.

What is the right way to assess whether the fiscal stimulus enacted in January 2009 had a positive impact? Start with common sense. When the government spends $800 billion on such things as highway construction, teachers and policemen who were about to be laid off, and so on, it has an effect. Workers who would otherwise not have a job now have one. Furthermore, they may spend some of their income on goods and services produced by other people, creating a multiplier effect.

Those who claim that this spending does not boost income and employment (or that it even hurts), apparently believe that as soon as a teacher is laid off, a new job is created somewhere else in the economy, or even that the same teacher finds a new job right away. Neither can be true, not with unemployment so high and the average spell of unemployment much longer than usual.

They also think that the government deficit drives up inflation and interest rates, thereby crowding out other spending by consumers and firms. But interest rates are rock bottom, even lower than they were in January 2009, while core inflation is running at its lowest levels since the early 1960’s. The conditions of the last four years - high unemployment, depressed output, low inflation, and low interest rates - are precisely those for which traditional “Keynesian” remedies were designed.

Economists’ more sophisticated forecasting models also show that the fiscal stimulus had an important positive effect, for much the same reasons as the common-sense approach. The non-partisan US Congressional Budget Office reports that the 2009 spending increase and tax cuts gave a positive boost to the economy, and indeed had the extra multiplier effects of the traditional Keynesian models. Allowing for a wide range of uncertainty [to allow for different economists' views], the CBO estimates that the stimulus added 1.5 percent to 3.5 percent to the level of GDP by the fourth quarter, relative to where it otherwise would have been. The boost to 2010 GDP, when the peak effect of the stimulus kicked in, was roughly twice as great.

To be sure, of the many theoretical models produced by eminent macroeconomists at prestigious universities, some say that fiscal stimulus has no positive effect on the economy, even under recent economic conditions. (The theoretical innovations underlyng the models have even won Nobel Prizes for the innovators, and not without justice.) But these models are not sufficiently realistic to meet the market test: they are not used by private businessmen for whom getting good forecasts matters to their planning and in turn to the success of their businesses.

Of course, econometric models do not much interest the public at large. A turnaround needs to be visible to the naked eye to impress voters. Given this, one can only wonder why basic charts, such as the 2008-2009 “V” shape in growth, have not been used - and reused - to make the case.

(Click here for larger graphs)