Inflation was the theme of this year’s international conference of central bankers in Jackson Hole, Wyoming. But, while policymakers are right to prepare for future risks to price stability, they did not place these concerns in the context of recent inflation developments at the global level – or within historical perspective.

CAMBRIDGE – Inflation – its causes and its connection to monetary policy and financial crises – was the theme of this year’s international conference of central bankers and academics in Jackson Hole, Wyoming. But, while policymakers’ desire to be prepared for potential future risks to price stability is understandable, they did not place these concerns in the context of recent inflation developments at the global level – or within historical perspective.

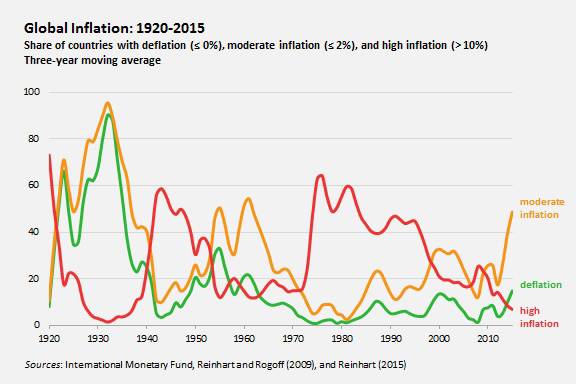

For the 189 countries for which data are available, median inflation for 2015 is running just below 2%, slightly lower than in 2014 and, in most cases, below the International Monetary Fund’s projections in its April World Economic Outlook. As the figure below shows, inflation in nearly half of all countries (advanced and emerging, large and small) is now at or below 2% (which is how most central bankers define price stability).

CAMBRIDGE – Inflation – its causes and its connection to monetary policy and financial crises – was the theme of this year’s international conference of central bankers and academics in Jackson Hole, Wyoming. But, while policymakers’ desire to be prepared for potential future risks to price stability is understandable, they did not place these concerns in the context of recent inflation developments at the global level – or within historical perspective.

For the 189 countries for which data are available, median inflation for 2015 is running just below 2%, slightly lower than in 2014 and, in most cases, below the International Monetary Fund’s projections in its April World Economic Outlook. As the figure below shows, inflation in nearly half of all countries (advanced and emerging, large and small) is now at or below 2% (which is how most central bankers define price stability).