Five years ago, Central and Eastern Europe was home to one of the world’s most impressive growth stories. But the region has struggled to regain momentum since the global financial crisis and subsequent recession, which suggests that a new growth model is needed.

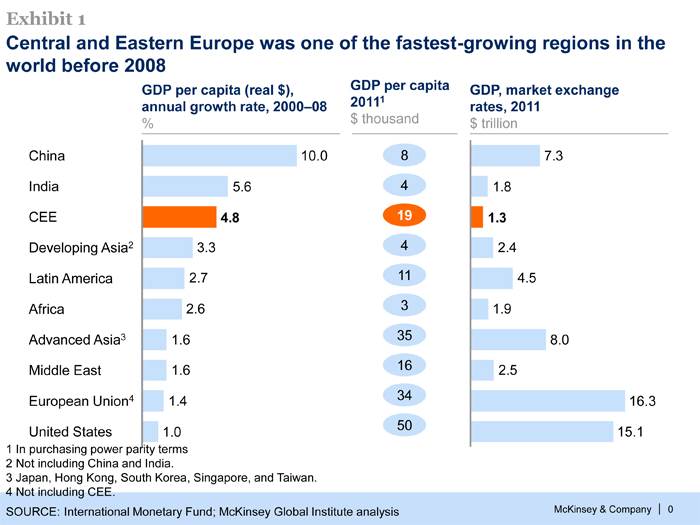

WARSAW – Five years ago, Central and Eastern Europe was home to one of the world’s most impressive growth stories. Annual GDP growth was close to 5%, just behind China and India. Foreign direct investment poured into Bulgaria, Croatia, the Czech Republic, Hungary, Poland, Romania, Slovakia, and Slovenia at a rate of more than $40 billion per year. One in six cars sold in greater Europe was being exported from factories in the region. Productivity and per capita GDP were rising briskly, narrowing the gap with Western Europe.

But the region has struggled to regain momentum since the global financial crisis and subsequent recession. Economic-growth rates have fallen to less than a third of their pre-crisis levels. Foreign direct investment, which plunged 75% from 2008 to 2009, has only partly recovered.

WARSAW – Five years ago, Central and Eastern Europe was home to one of the world’s most impressive growth stories. Annual GDP growth was close to 5%, just behind China and India. Foreign direct investment poured into Bulgaria, Croatia, the Czech Republic, Hungary, Poland, Romania, Slovakia, and Slovenia at a rate of more than $40 billion per year. One in six cars sold in greater Europe was being exported from factories in the region. Productivity and per capita GDP were rising briskly, narrowing the gap with Western Europe.

But the region has struggled to regain momentum since the global financial crisis and subsequent recession. Economic-growth rates have fallen to less than a third of their pre-crisis levels. Foreign direct investment, which plunged 75% from 2008 to 2009, has only partly recovered.